Features and Trends of Mobile Ecosystem Development in Eurasia

01.06.2026

Based on The Mobile Economy Eurasia 2026 report by GSMA

Eurasia currently demonstrates a number of key trends in the mobile industry development, such as active transition to digital and financial ecosystems for monetisation; strong imbalance in the adoption of 5G technologies and solutions across countries; and a strategic focus on technological sovereignty spreading from domestic network equipment to proprietary AI models and data centres.

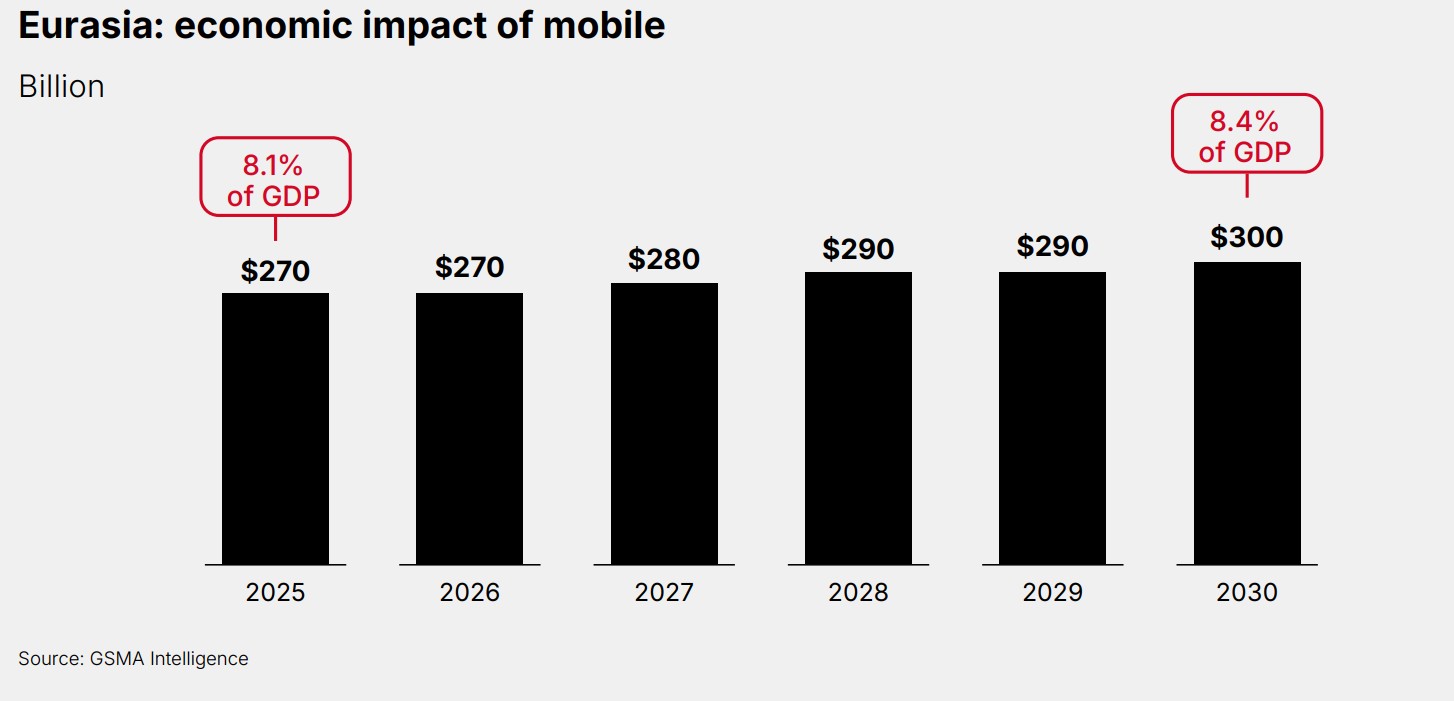

Mobile communications play a critical role in the Eurasian economy. According to GSMA forecasts, mobile sector share in the region’s economy will grow from $270 billion (8.1% of GDP) in 2025 to $300 billion (8.4% of GDP) by 2030 (Fig. 1 and Fig. 2). In 2025, the mobile ecosystem created about 750,000 jobs and generated $14 billion in tax revenue. At the same time, as the region's economic growth slows down, mobile technologies are becoming a driver of economic resilience.

Fig. 1 Mobile technology share in Eurasia's GDP, source: GSMA

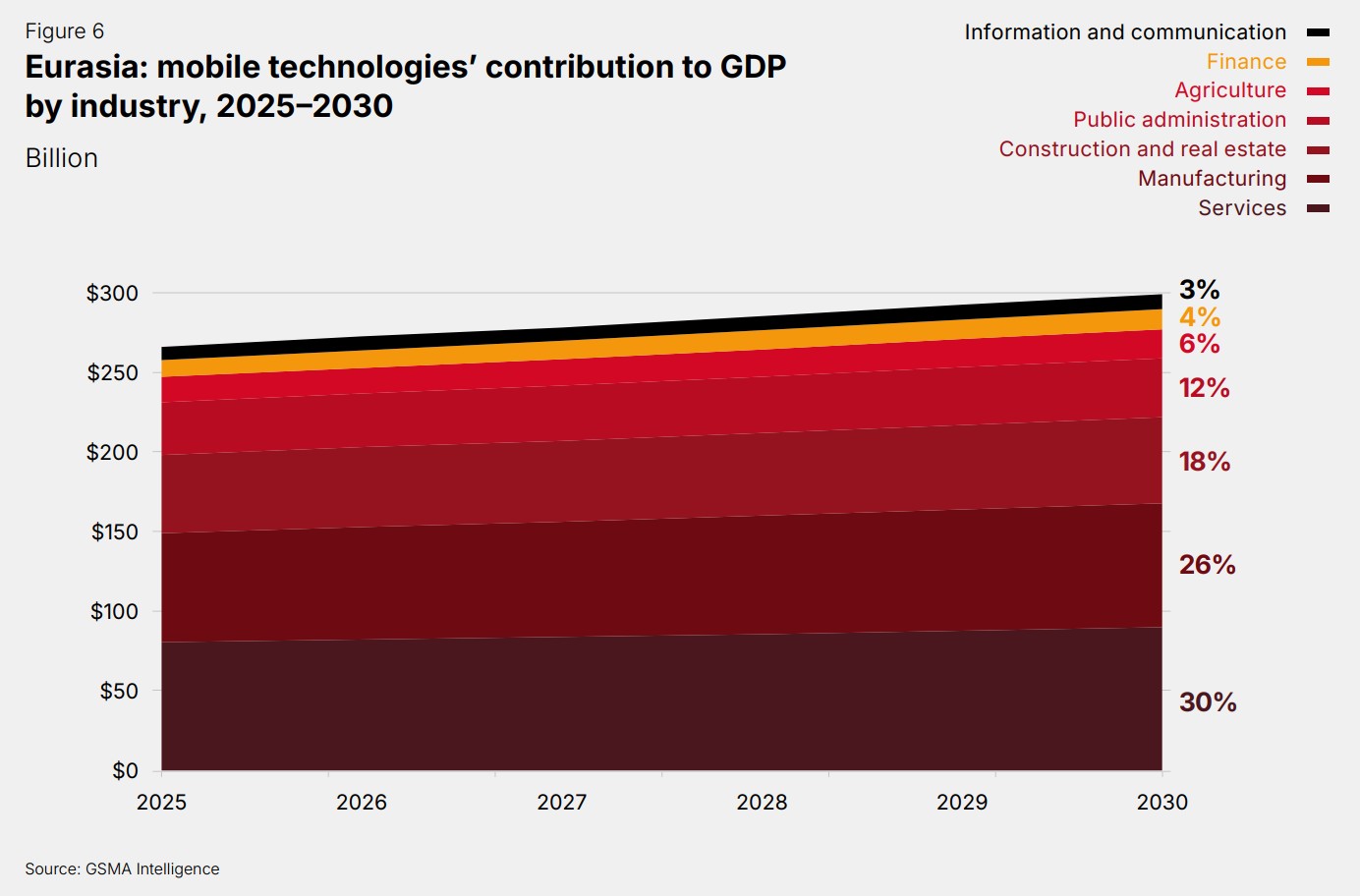

Fig. 2. Mobile technology share in GDP by industry, source GSMA

New monetization models

The development of new monetization models by operators and diversification of the operator business have become key trends in the mobile communications industry growth. Market players are actively capturing media, advertising, financial services, data centres, the Internet of Things, and smart city technologies for B2B and B2G, using artificial intelligence both for their own needs and to provide services to customers.

Today, the development of operator business in Eurasia is constrained by higher operation expenses and higher financing costs: growing revenues generally do not boost profits. For example, in Russia, operators showed double-digit revenue growth in 2025, but profits dropped due to higher depreciation costs driven by investments in digital projects. Operators see a solution for the current situation in diversifying their business beyond the communications services sector. Primarily, they offer packaged entertainment services: video, music, games, e-commerce and financial services. For example, Veon in Kazakhstan increased its multi-service subscriber base to 43.5 million (33.7% of all subscribers), accounting for 55.4% of customer-related revenue. And the churn rate in the segment is 50% lower compared to basic telecom services. Tcell in Tajikistan launched music and video platforms in Tajik and also in Dari, Pashto, and Urdu (partnership with Mawj Platforms). In Uzbekistan, Uztelecom integrated Alskom insurance products into its digital platform.

Financial services is another sector that operators are actively capturing in search of new growth opportunities. Operators are becoming digital “points of entry” to the financial infrastructure, mostly in the markets where such infrastructure does not exist as a unified ecosystem. In Kyrgyzstan, My O!, integrated with O!Bank, has grown from a telecom wallet into a versatile financial service supporting cards of all national banks, payments for public services, and etc. In Azerbaijan, Akart, Azercell's subsidiary, acquired an e-money license and integrated with Google Pay and Apple Pay. In Russia, MTS presented a prototype SIM-based payment technology that does not require Internet connectivity and integrates payment services, credit products, and other services. Operators are also actively involved in advertising and digital commerce. Subscriber data enables them to launch targeted advertising campaigns.

In the B2B sector, which is another area of business development and diversification, operators are actively investing in cloud services, data centres, IoT, cybersecurity, and smart cities. Rostelecom, through its mobile operator subsidiary, launched a high-capacity cloud cluster for virtual machines and big data. In 2025, the company's revenues from B2B/B2G grew by about 9% year-on-year. MTS launched MTS Web Services (MWS), a cloud platform. Viva Armenia has partnered with Oracle to boost its cloud and IT solutions for business.

Another promising growth point in the B2B sector is artificial intelligence, with the first AI-based offers already available in the market. MTS offered genAI-as-a-service as part of the MWS cloud platform (chatbots, knowledge bases, development tools). Azercell, together with GSMA Foundry and IBM, applied generative AI for automated drive test reporting and accelerated decision-making. In Kazakhstan, according to forecasts, companies' spending on AI will grow by about 11% per year in 2025- 2030. But currently, according to GSMA Intelligence survey data, the market perceives operators as telecom providers rather than advanced AI solution providers.

5G development process

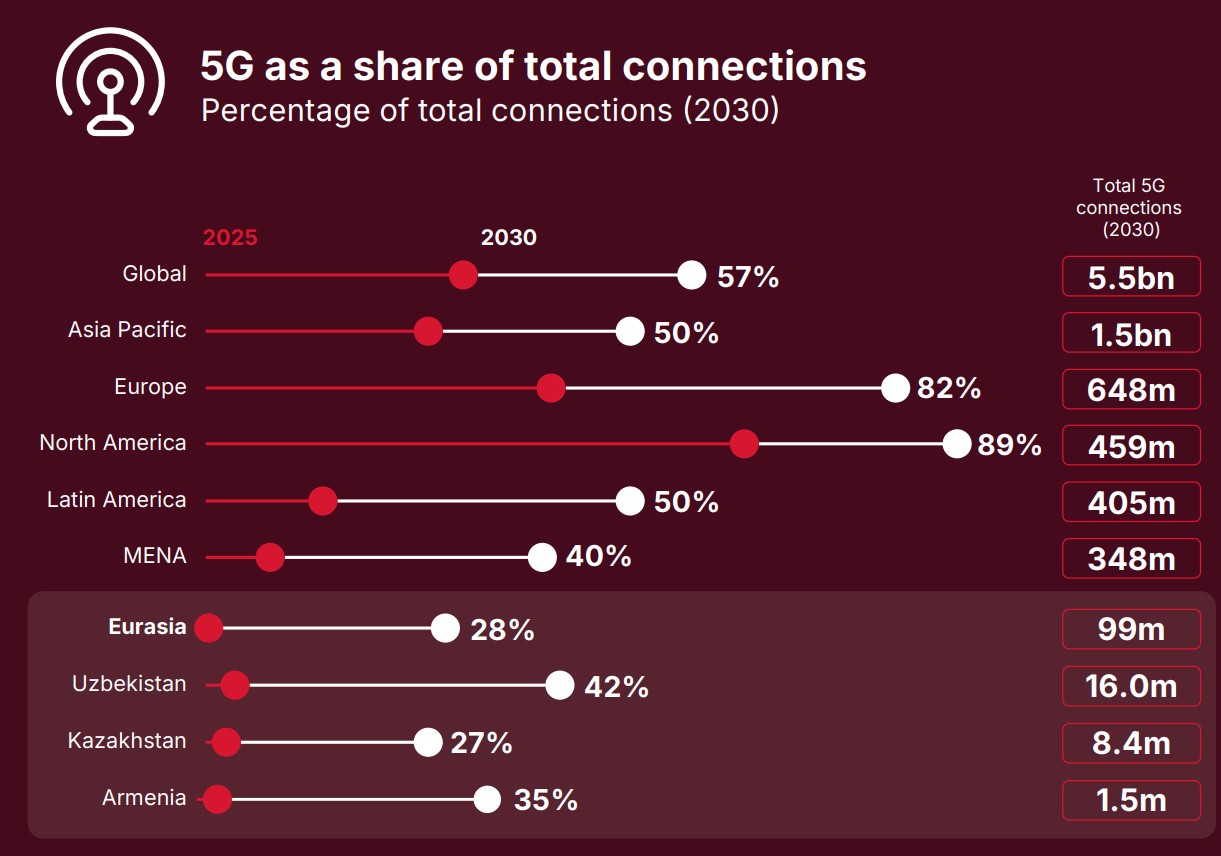

The transition to 5G in Eurasian countries goes different ways. The market features an obvious imbalance: while some countries are already transiting to active commercial use of networks, others are just starting to adopt them. In Armenia, Ucom has achieved 94% of 5G coverage: 47 cities, key transport and tourist routes, border crossings, and resorts. By mid-2025, Kcell installed 1,846 5G cell towers in 20 cities in Kazakhstan. In Tajikistan, 5G accounts for around 1%, and the government tasked the telecom industry with ensuring overall 4G coverage by 2027 and provide conditions for the transition to 5G by 2030 (Fig. 3).

Fig. 3 5G development in various regions, source: GSMA

A key factor influencing 5G development is radio spectrum provision. The sub 1 GHz band is critical for rural coverage, however, most Eurasian countries, excluding Armenia and Uzbekistan, have not yet allocated it. The 3.5 GHz and 6 GHz bands play a key role in boosting the throughput. To further develop mobile technologies and meet the requirements for growing traffic in the period up to 2035–2040, countries will require between 2 and 3 GHz in the mid-band, primarily in the key 3.5 GHz (3.4–3.8 GHz) band. Harmonization of the 6 GHz band at the World Radiocommunication Conference 2023 (WRC-23) offers opportunities for long-term investment planning.

Regulation can become an encouragement tool for operators: in Kazakhstan, from 2021 to 2025, the government offered the operators who invested in rural infrastructure an up to 90% discount for the frequency band.

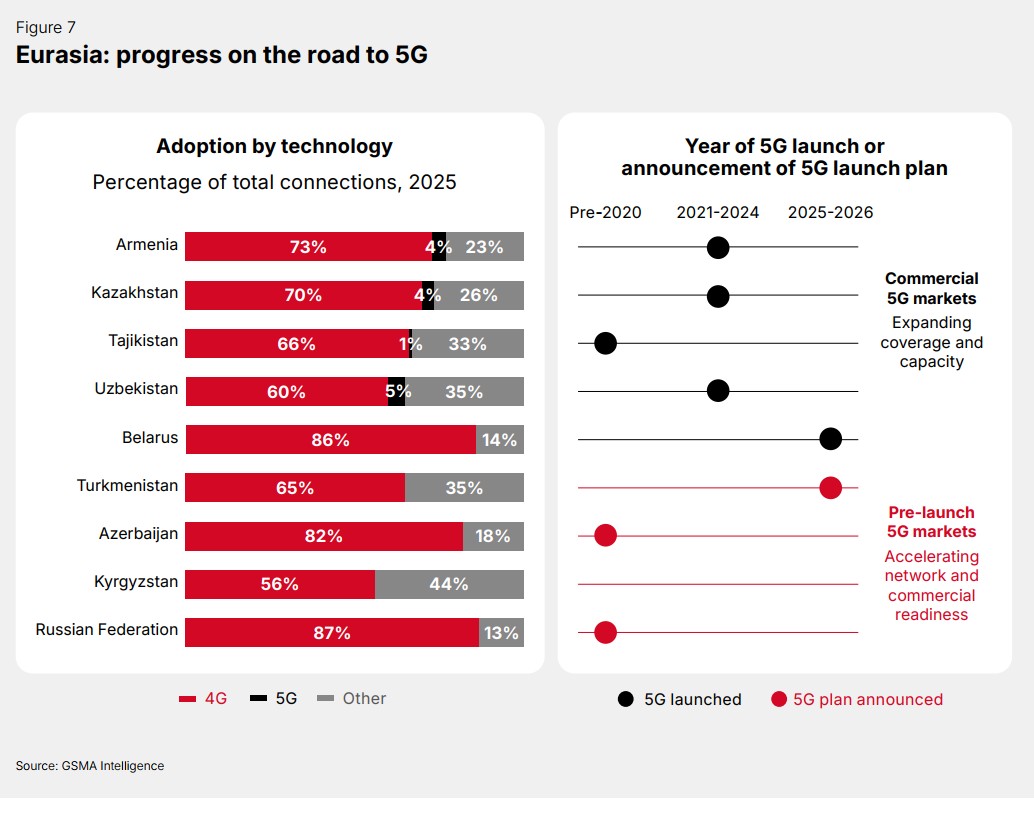

Along with 5G network expansion, investment and development of the 4G LTE network is underway, which is yet the basic technology for most users, covering over 50% of all connections in Eurasia (Fig. 5).

Fig. 5. 5G development in Eurasia, source: GSMA

Technological sovereignty

Digital technologies have become a key element in public administration and successful economic activity. The resilience and manageability of telecom infrastructure are becoming a priority, as network disruptions can seriously impact daily life, business, and national security. Technological sovereignty is becoming fundamental in boosting infrastructure resilience and building conditions for the long-term development of the digital economy.

The key priorities of technological sovereignty are: replacement of imported telecom equipment, development of national data centres and GPU clusters, creation of national LLM and agent-based AI solutions, and control over traffic routing and data.

Rostelecom in Russia has started country-wide deployment of domestic Bulat LTE equipment as part of its programme to bridge the digital divide. In 2025, MTS set to upgrade its backbone networks based on domestic equipment in 29 regions, expecting to boost the throughput capacity up to tenfold. In 2025, the company proceeded to install about 1,000 Irtea stations and introduced the first 5G cell tower from the same vendor.

Another aspect of technological sovereignty is data management. Azercell, Azerbaijan in cooperation with Amazon Web Services (AWS), deployed a hybrid cloud infrastructure combining the capabilities of international providers with the requirements of national data regulation. In 2025, Kyrgyzstan implemented a centralised model for routing international Internet traffic for the period from August 2025 to August 2026.

According to Implement Consulting Group estimates, AI may provide about 2% of GDP over the next decade, with approximately half of jobs supported by AI technologies. Therefore, an individual task is to build technological sovereignty in any activity and AI-related applications. In 2025, Kazakhtelecom launched the first Sovereign AI factory in Central Asia, deploying a GPU infrastructure for training and using large-scale AI models in the government and corporate sectors. Ucell, Uzbekistan launch construction of a 5 MW data centre to be used to host digital platforms and process AI workloads as the demand for computing resources grows.

Also, operators are implementing security systems that can also be seen as part of technological sovereignty reducing dependence on foreign cybersecurity solutions. The MTS Defender AI-powered system (Russia) blocked over 3.17 billion suspicious calls in 2025. Solar, Rostelecom’s subsidiary, has implemented network filtering tools to block fraud calls and malicious websites and identify data leak risks. In Kazakhstan and Uzbekistan, in 2025, operators introduced anti-spoofing systems, which can identify international calls disguised as local numbers.

Therefore, technological sovereignty in Eurasia is an overarching strategy that covers everything from cell towers and submarine cables to large language models and cybersecurity systems. Operators and governments are collaborating closely to mitigate external risks and at the same time build new economic potential.

The digital mobile ecosystem in Eurasia is a key driver of economic and social development and has a vast potential. Market players and government institutions clearly recognize the need to adopt advanced AI-based digital services and new technologies. Governments are trying to overcome development disparity and the lag in bridging the digital divide through government programmes and various regulatory levers.