D2D market: current state and future outlook

27.03.2026

Based on ITU reports “Measuring digital development: Global Connectivity Report 2025” (“Facts and Figures 2025” and “The State of Satellite Broadband 2025”, GSMA report “Spectrum for D2D Public Policy Paper”, GSOA webinar “The Game-Changer: Direct-to-Device Satellite Connectivity”, Analysys Mason webinar “From orbit to edge: satellite meets cloud in the age of AI”, ITU webinar “Direct-to-Device policy: Shaping the future of seamless connectivity” and World Satellite Business Week 2025 conference.

Currently, the direct satellite communication technology with the use of an unmodifiedsmartphone, Direct-To-Device (D2D, sometimes also called Direct-to-Cell), is one of the most discussed and dynamically developing trends in the satellite communications industry. The possibility to stay connected at any poinon the Et arth without using an expensive special phone handset looks extremely attractive. D2D systems are actively developing. They have already served as basis for providing texting services, and from this year on, the operators promise to enable voice and narrowband data transmission, too. However, the industry is still facing a lot of challenges: technical, economic, and most of all regulatory.

Imbalances in coverage with modern digital services

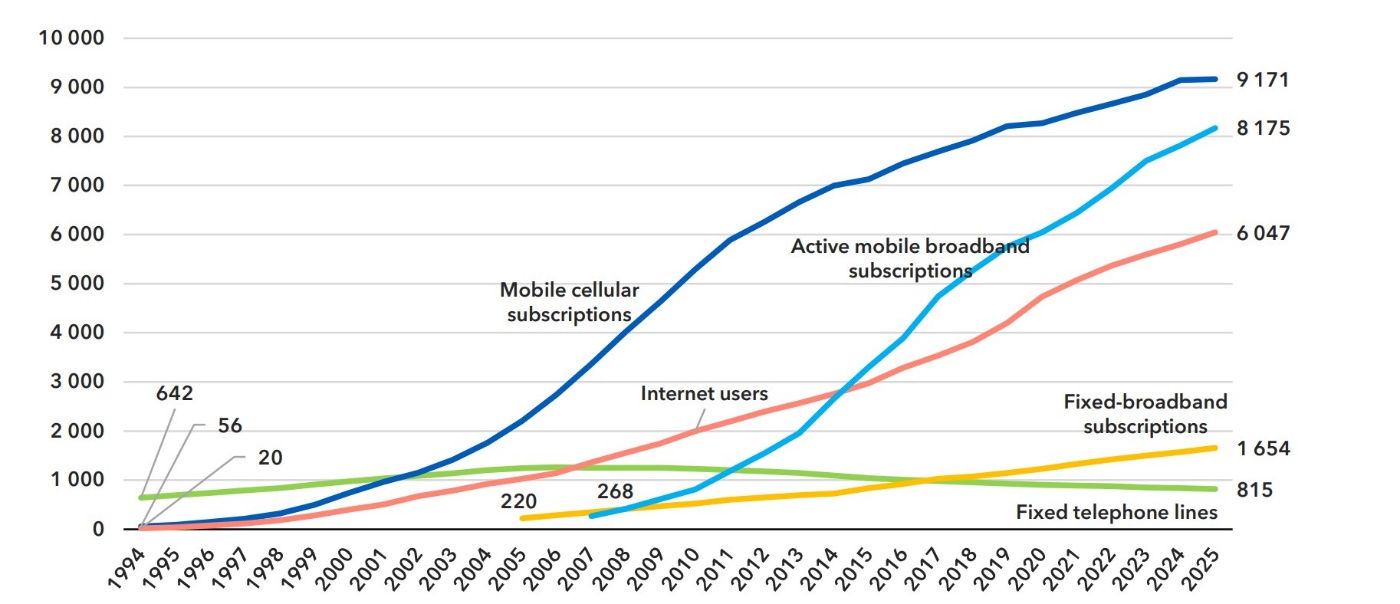

According to the International Telecommunication Union (ITU) [1], in 2025 the number of Internet users globally grew by more than 240 million people. 6 billion people are online, i.e. about three quarters of the Earth’s population. However, 2.2 billion people still remain unconnected (see Fig. 1).

Fig. 1 Evolution in selected connectivity indicators (millions). Source: ITU

Internet users are 94% of residents of countries with high levels of income, while in countries with low levels of income the figure is merely 23%. 96% of those who do not use the Internet live in countries with low- and medium-income levels. Among the urban population, the share of Internet users is 85%, while for rural areas this figure is 58% (see Fig. 2).

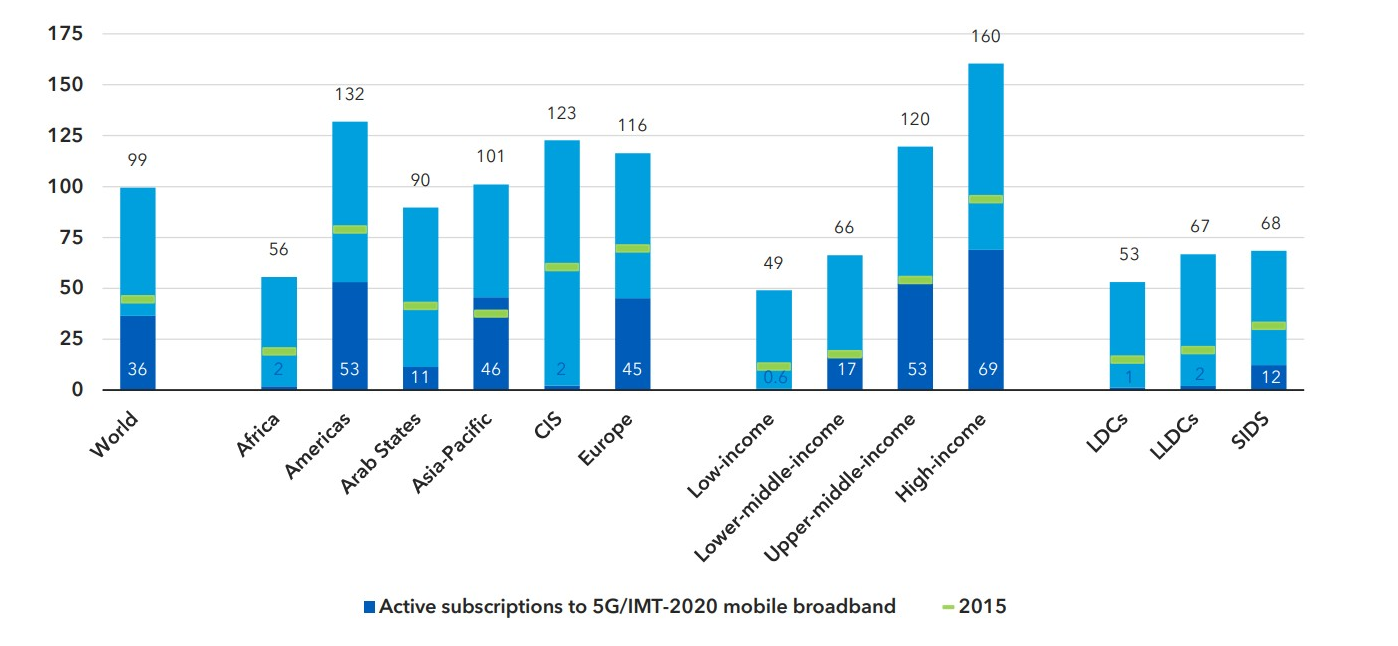

Fig. 2 Active mobile broadband subscriptions per 100 inhabitants by region, 2015 and 2025. Source: ITU

Globally, there are 99 subscribers per 100 inhabitants, but the indicators vary from 132 in the North and South Americas to 56 in Africa. The share of 5g users makes about one third – or approximately 3 billion – of all mobile broadband subscribers in the world. 84% of inhabitants in countries with high income levels and only 4% in countries with low-income levels have access to 5G.

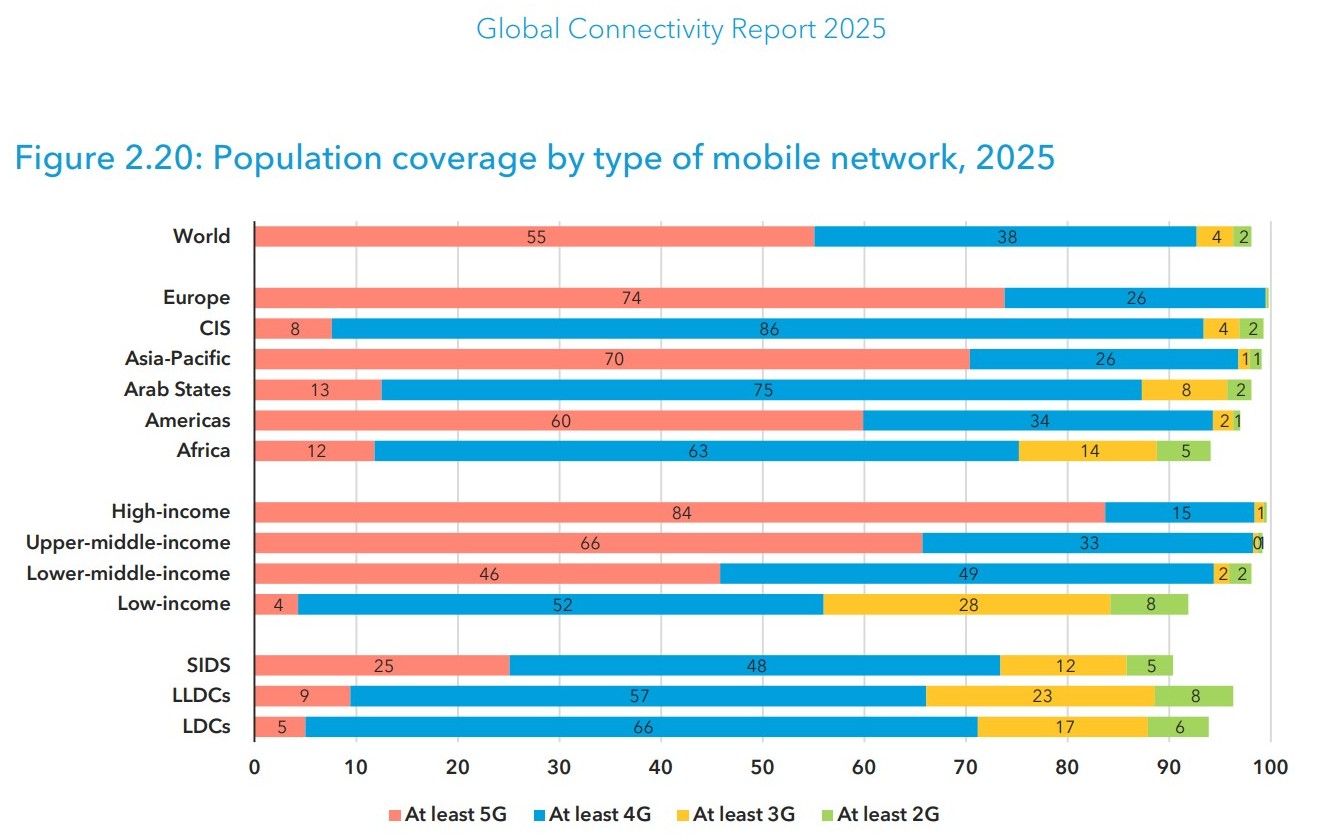

Today, 5G services cover 55% of the world’s population, but their spread remains irregular: In Europe, 74% of population is covered with 5G; in Asian and Pacific region, 70%; in the North and South Americas, 60%; in Africa, 12% (see Fig. 3).

Fig. 3 Population coverage by type of mobile network, 2025. Source: ITU

One of the efficient tools to expand the mobile Internet network coverage and level up the skew of their use – between different regions as well as between the city and the countryside – are satellite technologies.

Space technologies as a driver of enhancing global connectivity

Satellite technologies – their evolution and development – are now one of the decisive factors in creating a global information and communications ecosystem and universal connectivity. The main factors of affordability of space technologies are cutting costs for the launches and miniaturisation of the space-based systems. What used to be a specialised solution has now become a strategic tool to expand the access to connectivity services in the widest variety of conditions.

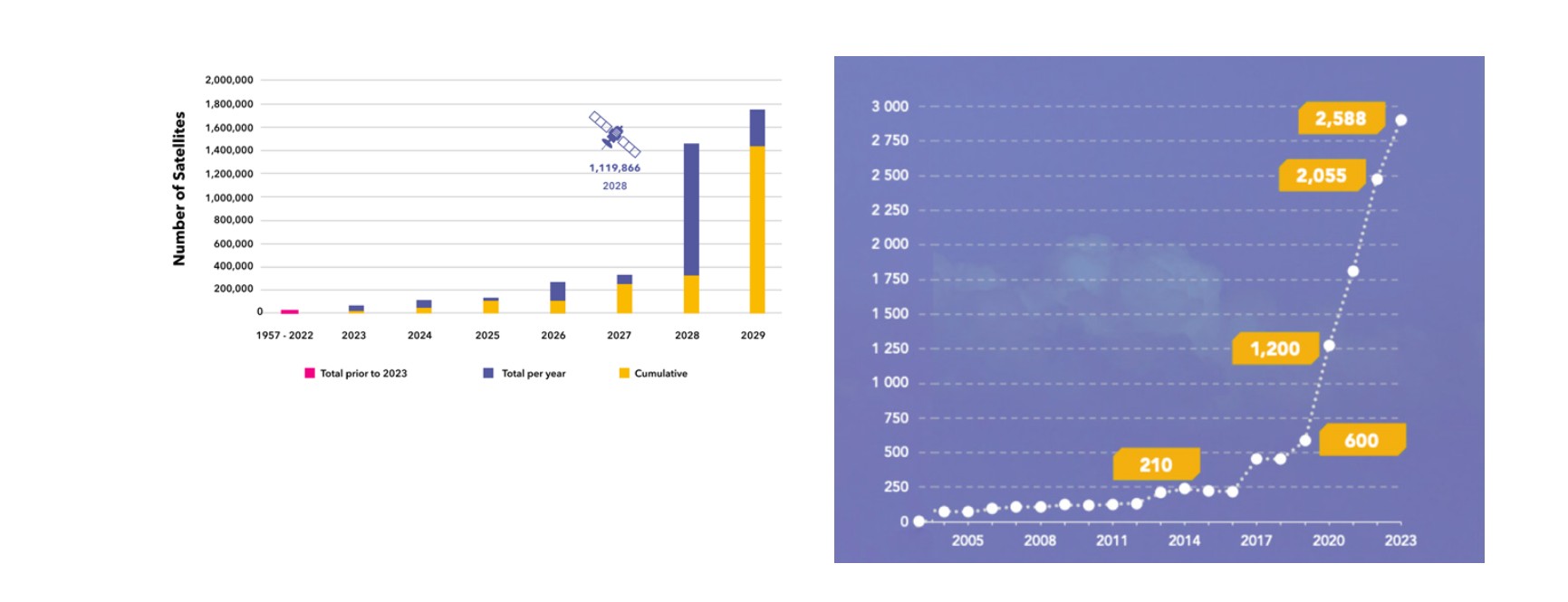

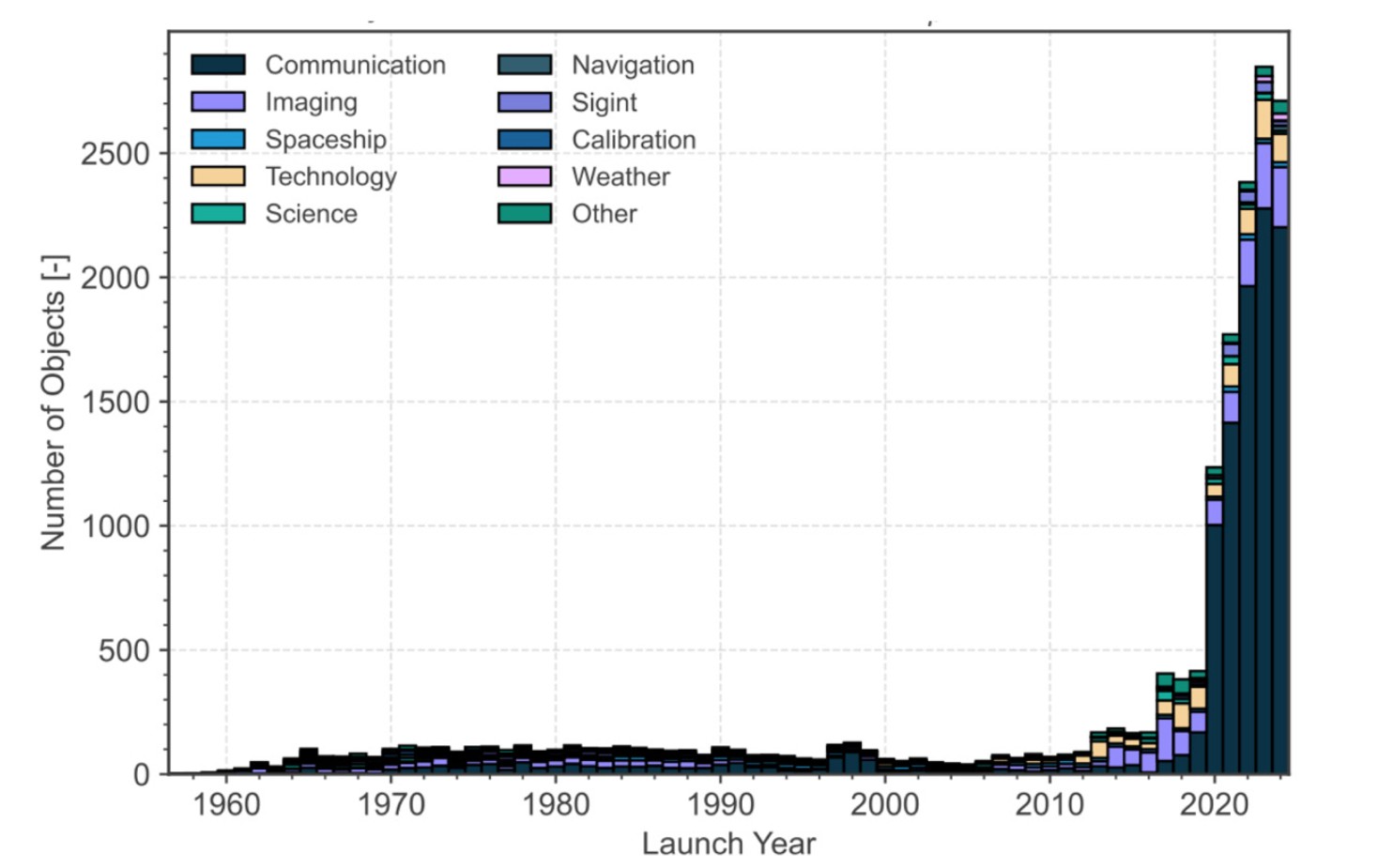

The quantity of satellites put to orbit has begun to increase exponentially (see Fig. 4).

Fig. 4. Number of satellite launches since 1957. Source: ITU

The left graph in Fig. 4 is the number of non-geostationary satellites for which member states have registered radio frequencies with ITU; the right graph is the number of space objects launched before 2023. According to the McKinsey research data on which** ITU is relying in its report “The State of Satellite Broadband 2025” [2], in the basic scenario, by 2030 there will be 27,000 active satellites operating in orbit. But there are other forecasts, too: Satellite Today assumes that by 2030 the number of active satellites may reach 50,000, most of them in low orbit (Fig. 5).

Fig. 5. Payload launch to 200-1750 km altitude, 1957-2023. Source: ITU

The overwhelming majority of satellites operating in orbit today are communication satellites. The outstripping development of the satellite communications, compared to other space industry sectors, is in many ways attributable to the fact that high-speed reliable communications are the basis for other services, first of all Earth surface monitoring. Besides, broadband communication has been practically recognised as a basic human need. Formation of mega-satellite communication constellations has led to communication satellites dominating the orbit. Plans of operators to develop the existing constellations and bring up new ones suggest that this status quo will remain for a long time to come.

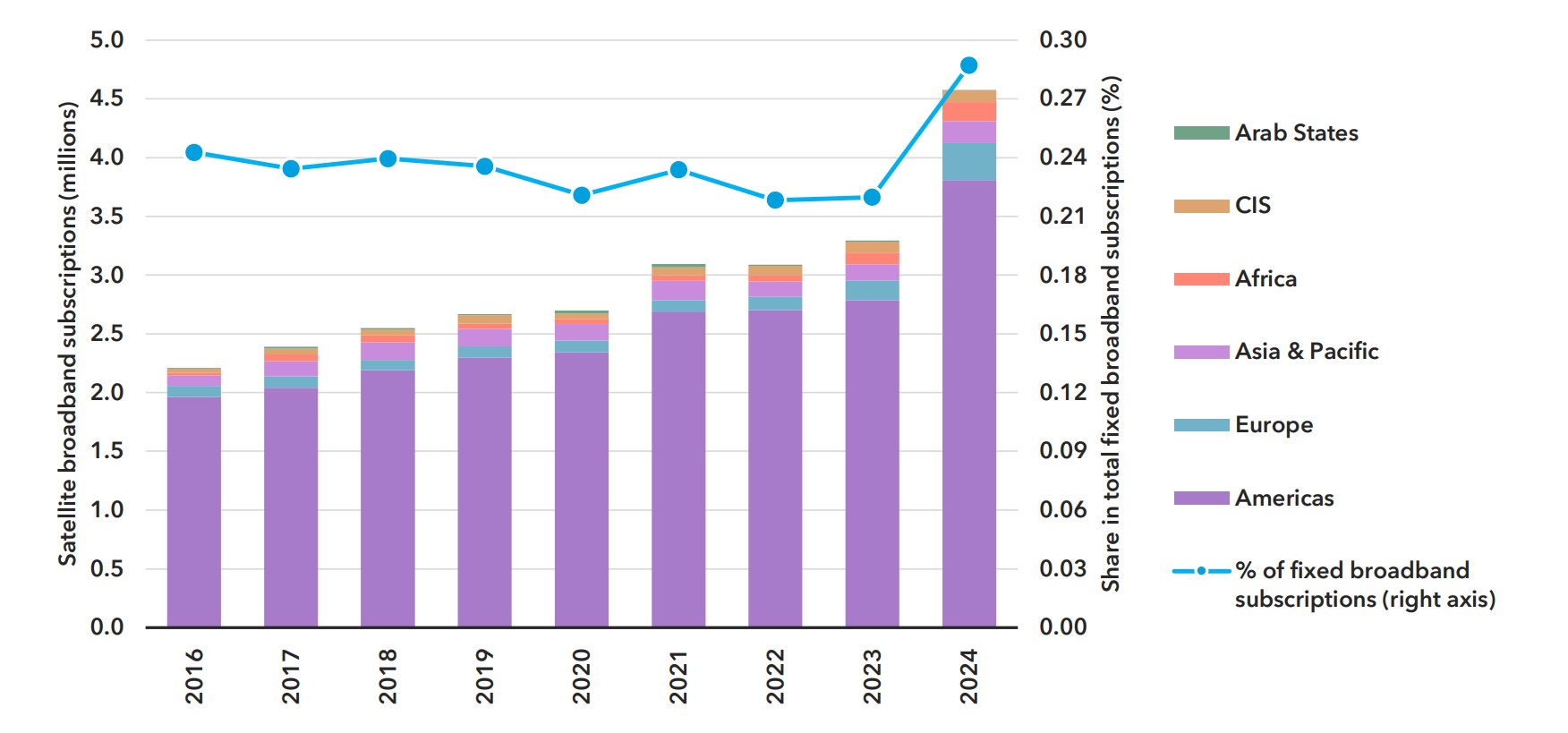

The world witnesses the steady growth in the number of broadband satellite connectivity users, which has gained momentum in 2024 when 1.1 million new satellite subscribers were registered. Nevertheless, the satellite connectivity penetration is still not sufficiently high – less than one satellite access subscriber per 1,000 inhabitants (Fig. 6).

Fig. 6. Evolution of satellite broadband subscriptions. Source: ITU

More than 80% of all satellite broadband connections are on the American continent. They are clustered mostly in the USA, Brazil, Mexico, and Argentina.

Development of standards and introduction of non-terrestrial networks (NTN) into the 3GPP project plays an important role in integrating satellites with 5G and 6G ecosystems. The strive to create large satellite constellations spurs the chase of launching Direct-to-Cell or Direct-to-Device (D2D) services.

Experts of Analysis Mason consultancy believe that none of the players will be unconditional winner on the D2D market due to challenges associated with regulation, frequency spectrum use, and the not quite understandable business model. ITU, with reference to Juniper Research, presents the following figures: according to the results of the year 2025, commercial D2C services will yield $30M; by 2029, the income from D2C will grow to $1.7B.

Frequencies for D2D

Frequency allotment is the main factor of success of any satellite communications project. And on various forums dedicated to D2D this factor has been voiced and emphasised more than once.

Radio Regulations is an international treaty that regulates the global use of the radio frequency spectrum and satellite orbits and contains provisions on coordination and registration of frequency assignments.

The agenda of ITU’s forthcoming 2027 World Radiocommunication Conference (WRC-27) includes more than 14 items concerning regulation of space service operations. D2D/D2C technologies will be discussed at WRC-27 within the framework of item 1.13 on the agenda, which will cover the research on the possible new allocation of mobile satellite communication services to ensure direct links between satellites and user equipment of international mobile telecommunications (IMT) in addition to the terrestrial IMT network coverage. A possibility of creating an international base to facilitate development of D2D services will also be discussed.

ITU regularly updates the specifications of various generations of IMT (4G, 5G), and in 2020 it began working on IMT-2030 (6G). The ITU-R recommendation says that interaction of terrestrial IMT-2030 network with non-terrestrial networks (NTN), including satellite communications and repeaters on high-altitude platforms, will improve the required connectivity tasks.

Today, D2D services operate in two parts of radio spectrum: 1) frequency bands defined for IMT and dedicated to mobile service; 2) frequency bands dedicated to mobile satellite service (MSS).

D2D in IMT spectrum

Utilization of the mobile communication spectrum offers obvious advantages. First: the transmission band is considerably larger than that coordinated for MSS. But there is also the underside here: the spectrum is used by mobile communications operators who will not tolerate interference from satellite services. Second: a huge market of potential subscribers and a vast number of customer devices. Yet here it’s not all roses, too: the emergence of a massive market of smartphones with D2D function is still far away.

Licensing of D2D service operating in IMT spectrum [3]

A D2D operator who provides services in IMT spectrum ranges works under the license of a mobile network operator (MNO). The rights to use a satellite of any terrestrial range must ensue from the exclusive rights of the MNO to that spectrum. In this case, the MNO is responsible for preventing interferences to other services. It also decides which parts of the spectrum to provide for D2D and under what licenses to do this (if different portions of the spectrum are regulated by different licenses).

Regulators should not give separate licenses to D2D operators for the same frequencies and regions as the existing MNO licenses. This approach, as the authors of the GSMA report believe, would undermine the regulatory ecosystem, which is now supporting investments into the mobile terrestrial infrastructure and into services for billions of users. Access to MNO spectrum for D2D should be based on the rights of the MNO license rather than any separate license from a regulator.

IMT protection

D2D using the IMT spectrum must protect IMT networks, according to the Radio Regulations. For example, in US, the regulator’s resolution demands that D2D services are provided on secondary base: they must not interfere with the operation of mobile communications services, but they are not themselves protected from interference. The GSMA’s position implies that at WRC-27 any new allocation of the MSS in the frequency bands defined for IMT should be made on secondary basis. Even if some country’s regulator allows D2D services to operate in the IMT spectrum, it has to ensure protection of the mobile communications services in the neighbour countries who have licenses to operate in the same range. That is why some experts [4] think this approach is inapplicable for Europe.

D2D in MSS spectrum

In countries where D2D services operating in MSS spectrum are allowed by the national regulator, these are already protected from interference by the Radio Regulations. Several ranges defined for MSS are already standardised by 3GPP:

- n254: 1610-1626.5 MHz and 2483-2500 MHz;

- n255: 1626.5-1660.5 MHz and 1525-1559 MHz;

- n256: 1980-2010 MHz and 2170-2200 MHz.

This has become an important step towards converging satellite and mobile communications but still does not warrant that mobile phone manufacturers will ensure operation in those ranges. Affordability of the phones to mass user is one of the priority challenges that has to be tackled by D2D players operating in MSS spectrum.

Discussion of new assignments for MSS at WRC-27

WRC-27, within the frameworks of agenda items 1.12 and 1.14, will be discussing the possibility of MSS operations in the following ranges:

- 1427-1432 MHz;

- 1645.5-1646.5 MHz;

- 1880-1920 MHz;

- 2010-2025 MHz;

- 2120-2170 MHz.

All these frequency ranges, except 1645.5-1646.5 MHz, are allocated for IMT. Any deployment of new mobile satellite communication services, including D2D, should protect the existing IMT identification in accordance with the Radio Regulations.

Item 1.13 of the WRC-27 agenda will offer discussion of the spectrum in the range of 694 MHz to 2.7 GHz, which is allocated to the mobile communications service and has its IMT identifier.

Item 1.14 on the WRC-27 agenda will consider the frequency band of 2010-2025 MHz, which is used for mobile communications in some countries of the EMEA and APAC region. Frequency ranges 1920-1980 MHz, 2110-2170 MHz, 1710-1780 MHz and 2110-2180 MHz are used for mobile communications all over the world.

For all aforementioned cases, GSMA insists on the maximum protection of IMT (according to the Regulations). Obviously, representatives of the mobile communications industry will defend their interests at WRC-27. In addition to everything listed above, the GSOA webinar “The Game-Changer: Direct-to-Device Satellite Connectivity” also mentioned a possibility to provide D2D services in C-band.

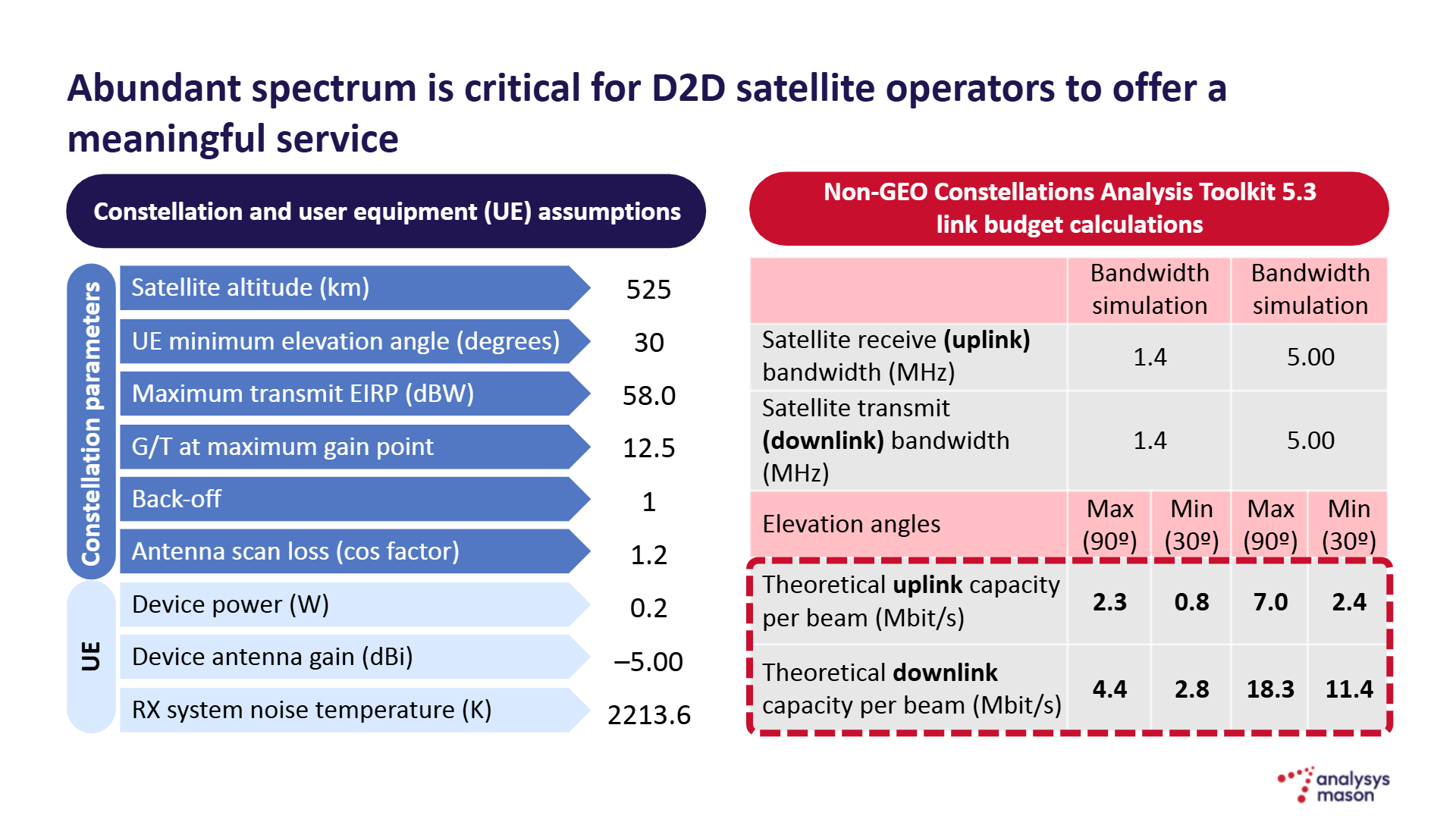

Beam capacity [5]

The size of the band provided to a satellite service directly defines the transmission rate offered to the subscriber. Experts of Analysis Manson consultancy have calculated the beam capacity of a notional D2D system (Fig. 7).

Fig. 7. Beam capacity calculation. Source: Analysis Mason

For this example, data of one newly designed satellite system were used. The data are shown in the left table in Fig. 7. The right table shows the calculation of the beam capacity, which is 18.3 Mbit/s at the most favourable conditions.

D2D as a business

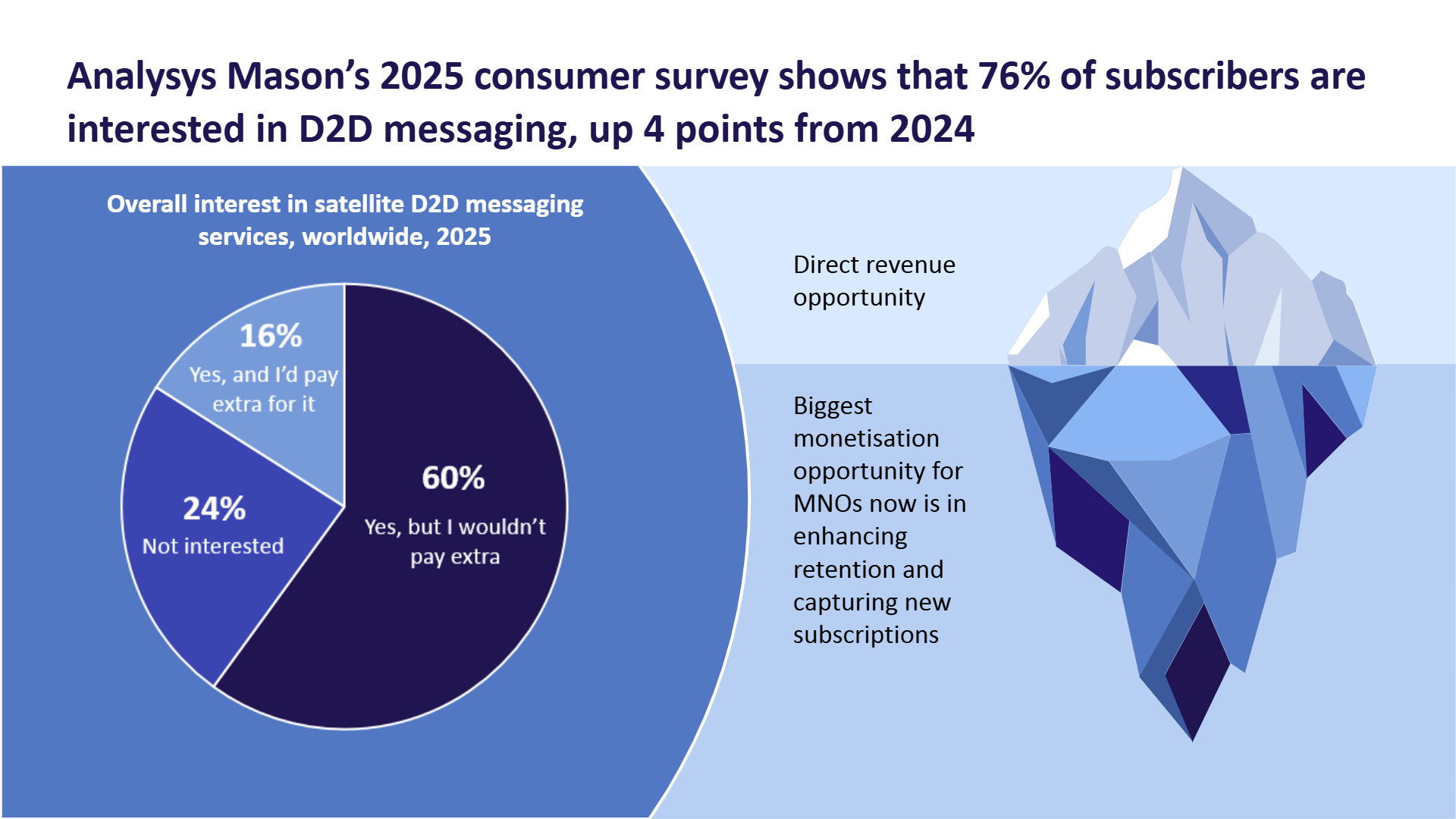

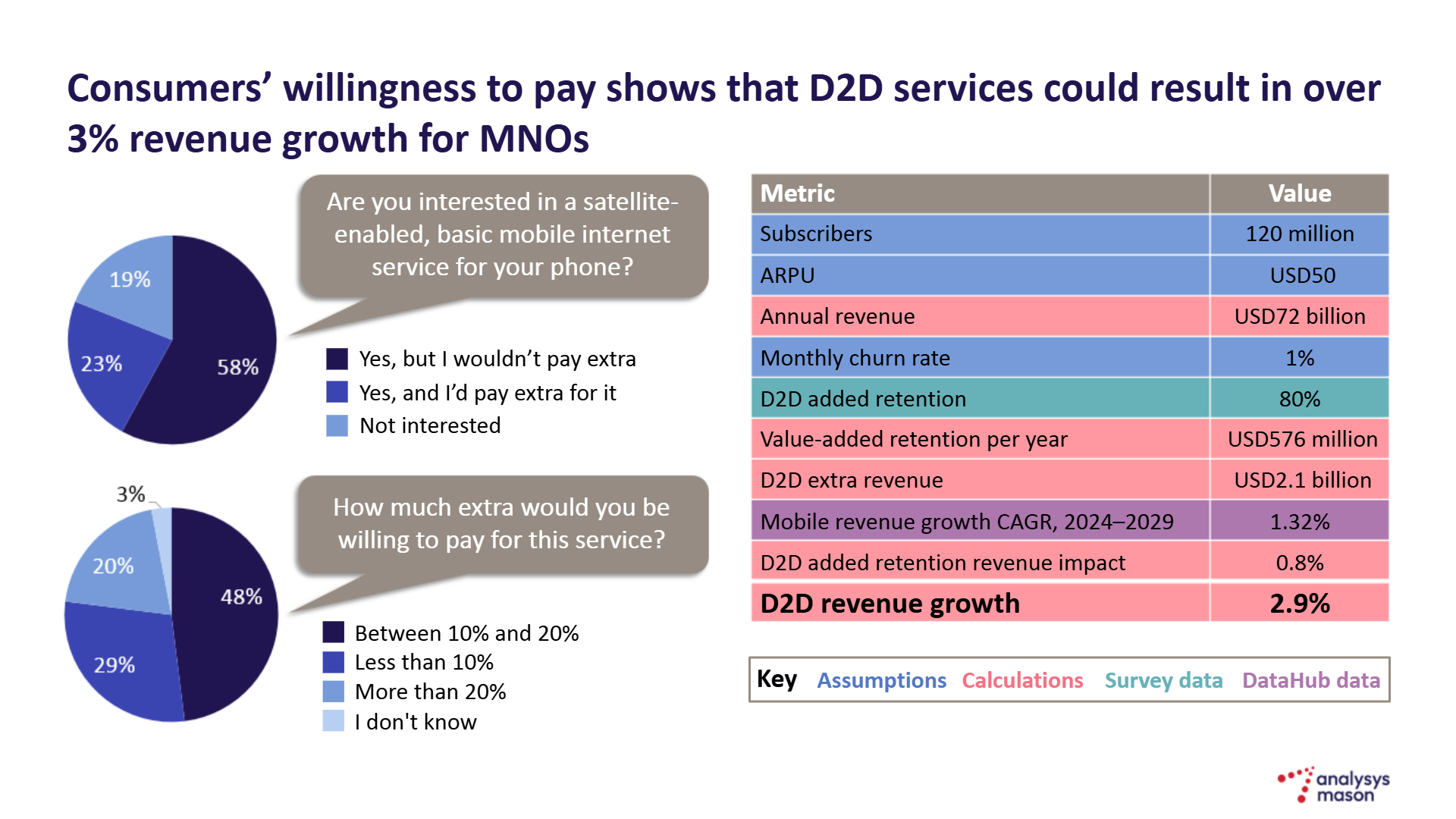

According to Analysis Mason industry survey, 77 MNOs have already launched D2D or are planning to do it soon. 76% of subscribers are interested in exchanging messages via satellite, but only 16% are ready to pay. So today D2D services are not a source of income but a mechanism to retain subscribers (Fig. 8).

Fig. 8. Analysis Mason polling data

The experts who participated in GSOA webinar “The Game-Changer: Direct-to-Device Satellite Connectivity” agree with this statement of question. However, they believe that the key D2D consumers, who will push evolution of the service, are public customers, such as emergency response agencies, fire brigades, etc.

But 48% of subscribers among those who are ready to pay for D2D agree to spend on that service from 10% to 20% of the tariff cost. Analysys Mason makes the following calculations: if we assume that some MNO has 120 million subscribers and the ARPU is $50, then D2D will be able to generate $2.1M per year, which is 2.9% of the total revenue (Fig. 9).

Fig. 9. Estimate calculation of D2D income based on Analysis Mason poll

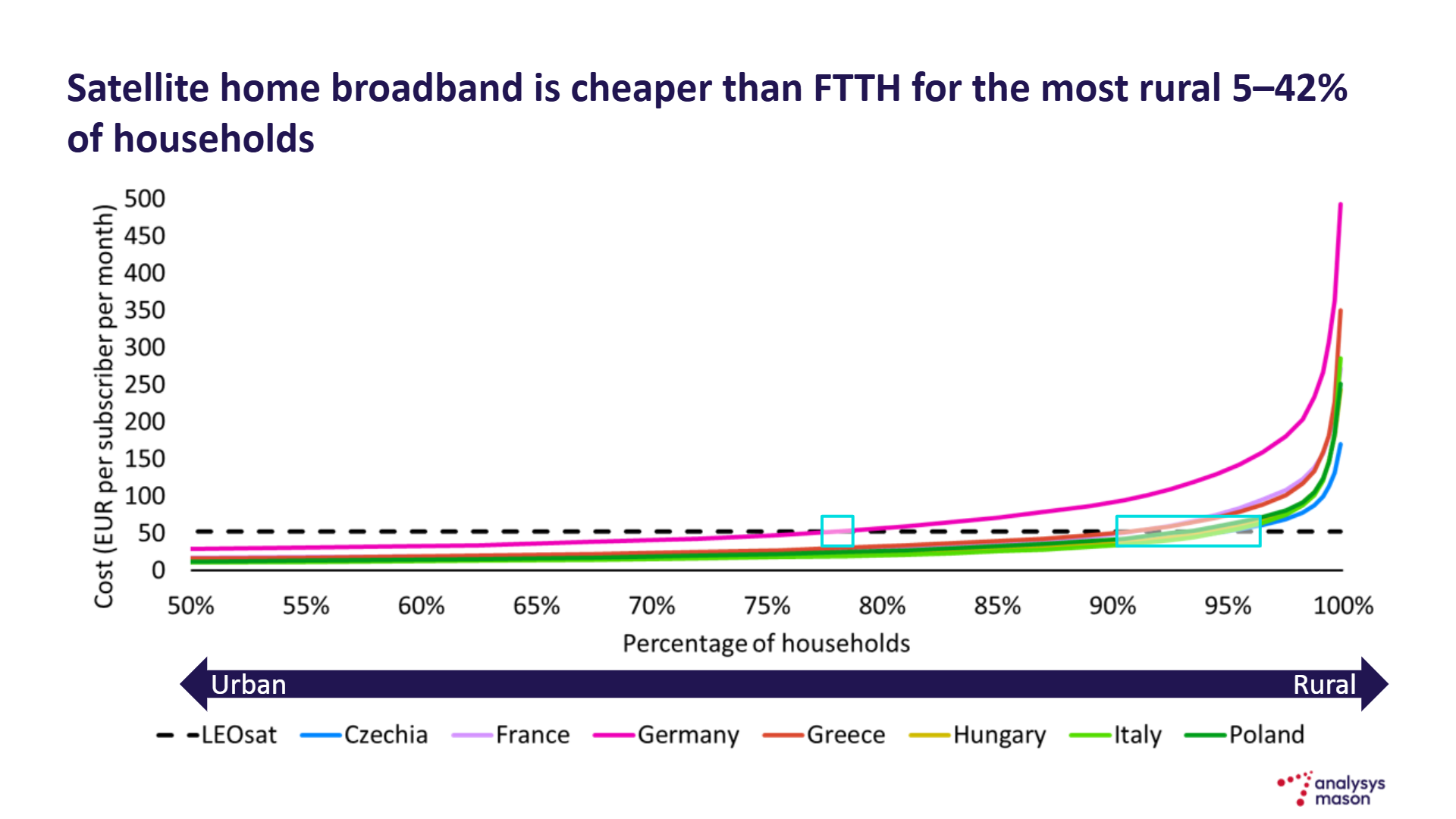

Let’s consider the price trends of the broadband connection via fibre optics and satellite depending on the location of subscribers in some European countries (Fig. 10). The blue rectangles are the area where satellite becomes cheaper than optical fibre. The result: 17 to 35 million homes in Europe where satellite communications beat optics in terms of the price.

Fig. 10. Comparative prices of optical fibre and satellite broadband access depending on remoteness from the city. Source: Analysis Mason

D2D projects

Today, several D2D projects are being implemented both by legacy players and by startups. Generally, a service of text message transmission is provided, but already from 2026 on, the operators promise to begin commercial operation of voice and narrow band data transmission.

AST SpaceMobile

The operator is planning to start commercial operation of the system in 2026 and is actively developing its satellite constellation. To the six satellites already in orbit – one Bluewalker-3 and five BlueBirds – one more was added in December 2025, and the other one is planned for launch in Q1 2026. As Scott Vishnevsky, Director General of AST, stated at WSBW-25 conference, the use of big satellites is one of the key strategies of the company. The size of a phased antenna array on previous generation satellites BlueBird 1-5 is over 60 m2; on next generation satellites BlueBird 6 and 7 is over 200 m2. The declared peak transmission capacity of these satellites is 120 Mbps. AST assembles its satellites at its own factory.

Originally, AST SpaceMobile was working within the strategy of using terrestrial mobile communications frequencies and signed an agreement with AT&T on the use of frequencies. In June 2025, the operator got the rights to use the 40 MHz L-band in the USA and Canada, which Ligado had earlier rented from Inmarsat.

In August 2025, AST acquired from ITU the 60 MHz S-band: 1980-2010 MHz and 2170-2200 MHz. The special value of that acquisition is that these 60 MHz are coordinated in the entire world for the provision of MSS services.

So, AST is becoming a D2D service operator, working in the frameworks of both strategies: using the IMT spectrum of partner cellular operators and using the spectrum allocated for mobile satellite communications. In June 2025, AST and Vodafone – one of AST’s investors – set up a joint venture called SatCo. And in November 2025, the partners declared that they intended to create a European satellite constellation of secure communications.

Globalstar

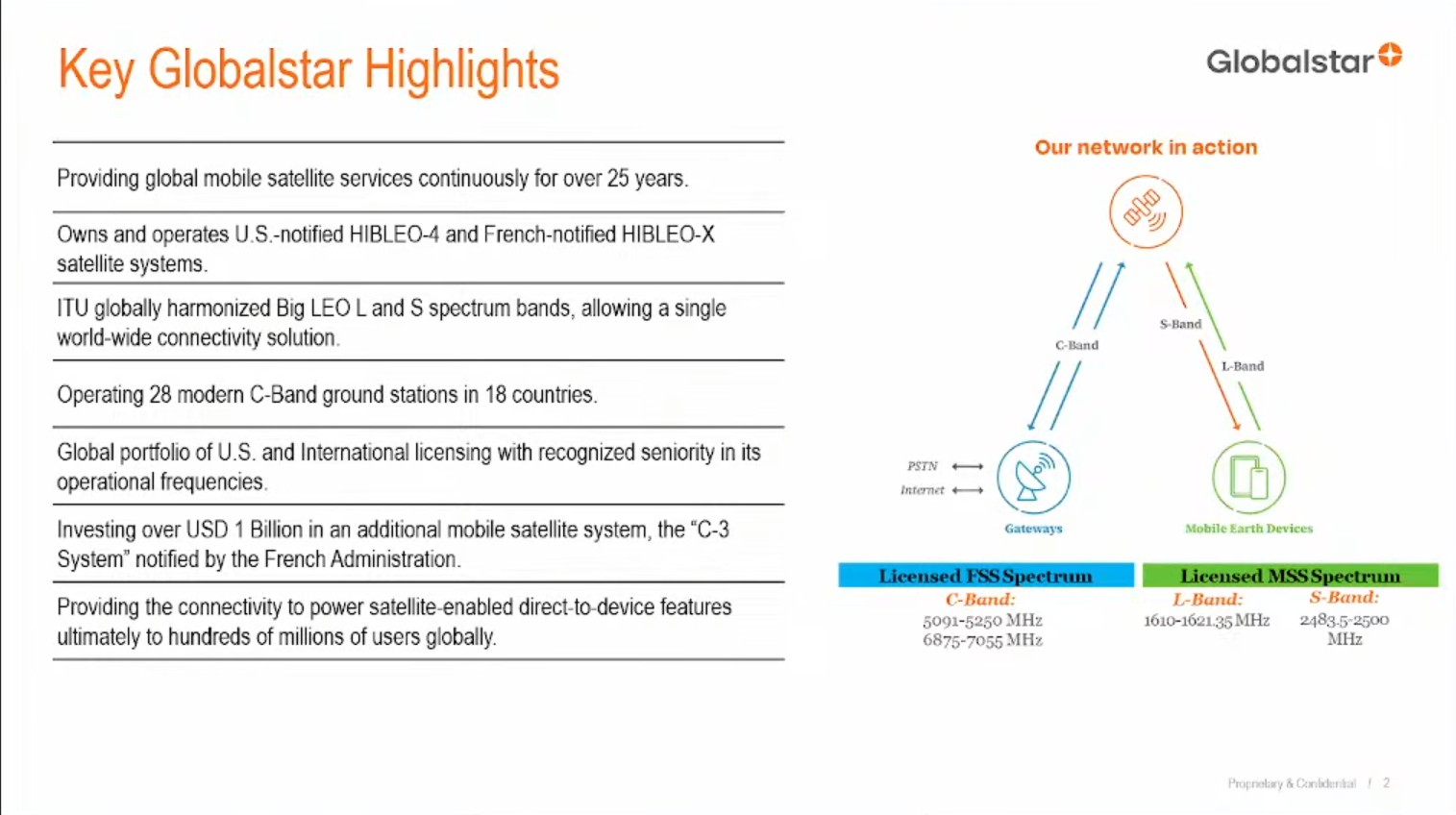

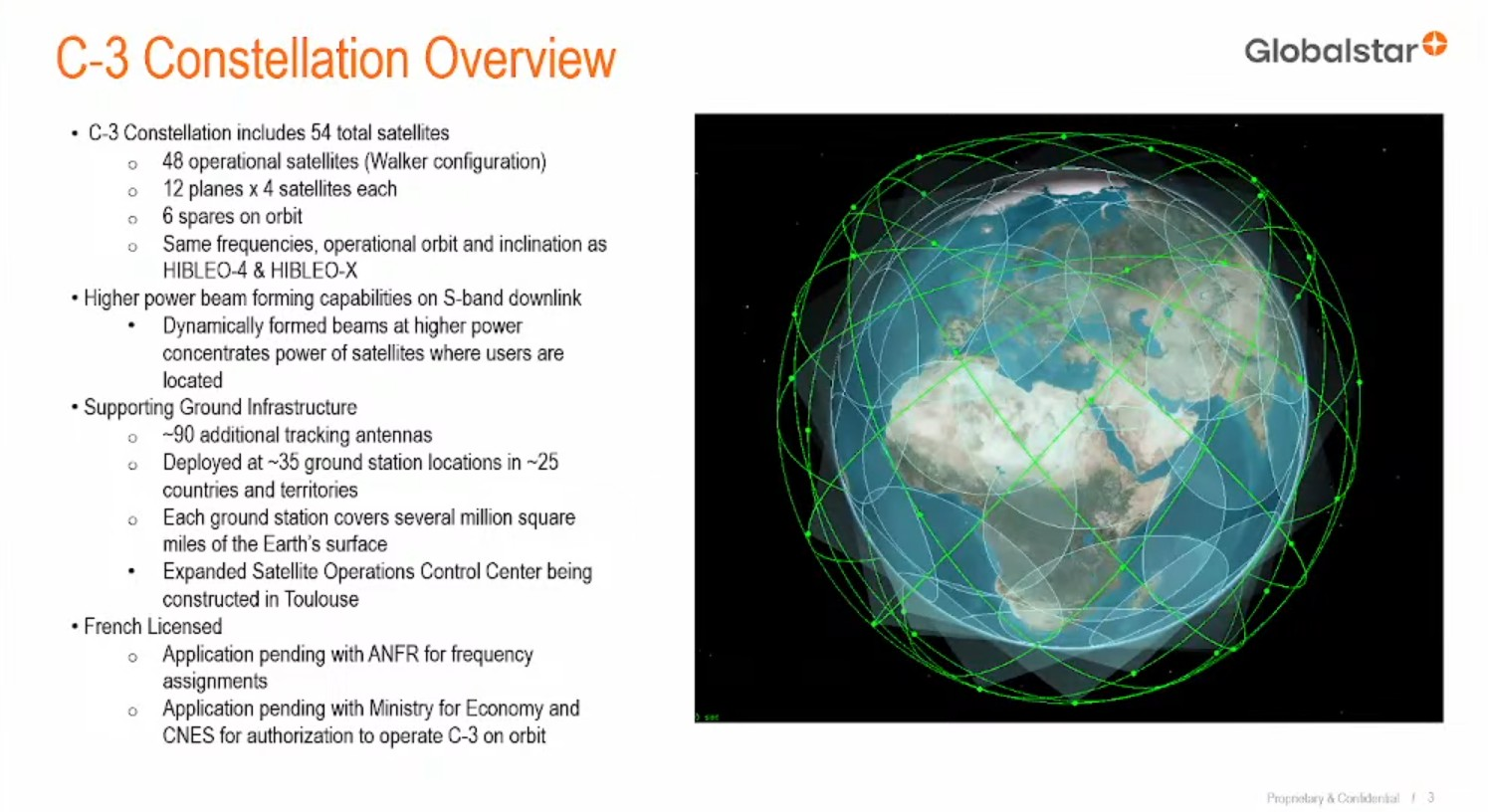

Thanks to cooperation with Apple, this operator obtained funding to renovate its constellation in an amount of $1.5B and is getting ready to start launching in the nearest time. To the same orbits where the existing constellation resides – 1414 km in altitude – 48 existing and six standby satellites will be placed (detailed information about the Globalstar system and outlooks of its development is given in Fig. 11 and Fig. 12).

*Fig. 11. Globalstar system condition. Source: ITU1 * [6]

Fig. 12. Globalstar system development outlooks. Source: ITU

Also, as part of expansion of the constellation’s capabilities, it is planned to create 90 gateway stations around the globe.

Iridium

This operator works in L-band, and its main service is Internet of Things (IoT). In 2024, Iridium CEO Matt Desch declared that the company would develop its D2D services within the frameworks of 3GPP standards, seeing that as the most beneficial strategy. In September 2025, the operator declared the launch of the Iridium NTN Direct service, which offers IoT services consistent with 3GPP standards. Vodafone intends to integrate this service in its service package.

Lynk Global

Lynk Global, who sought MNO partners all over the world, also managed to get a global resource of frequencies for MSS as it united with Omnispace, another startup creating D2D system. Once the merge is finished, the major stakeholder of the newly born company will be the satellite operator SES. The ex-competitors in D2D, Lynk and Omnispace, declare that the goal of their combination of efforts will be assistance to the reliable deployment of D2D services and Internet of Things for mobile network operators (MNOs), corporate and governmental customers, within the framework of a multi-orbit network architecture with several spectra. The combined company will use 60 MHz of globally coordinated spectrum in the S-band owned by Omnispace and the priority requests to ITU optimised for D2D services. The licensed spectrum of mobile satellite communications of Omnispace corresponds to 3GPP standards for non-terrestrial networks.

Space 42

In November 2025, the operator put into commercial operation the satellite Thuraya-4, which provides mobile communication services in L-band. The area covered by the satellite includes, as the operator stated, over 100 countries in Europe, Africa, Central Asia, and Middle East.

At WSBW-25, Viasat and Space42 offered a new approach to the D2D market, based on the joint use of the spectrum and on seeing satellites as shared infrastructure, like cellular communication towers. To implement this concept, the operators created a joint venture named Equatys.

Viasat and Space42 place Equatys’s disposal 100 MHz of coordinated MSS spectrum and a space segment: satellites of Thuraya-4 and Inmarsat constellations. Plans are made to create a proprietary LEO constellation. The partners emphasize that Equatys is a system that is open for everyone.

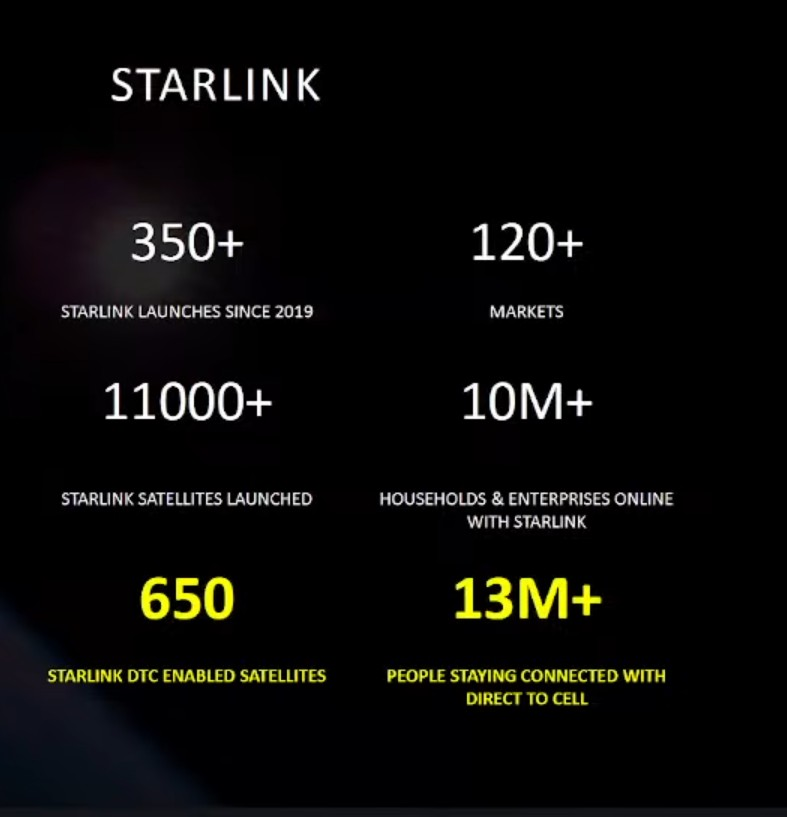

SpaceX/Starlink

From 2019 to February 2026, the company made over 350 launches of the Starlink satellites (Fig. 13). Currently, satellite broadband services are provided in more than 120 countries. Starlink has about 650 Starlink Direct to Cell satellites. They provide service to T-Mobile (in the USA) and other mobile network operators, using the spectrum under shared use agreements. The D2D service is provided by the operator in 12 countries. In November 2025, the company launched D2D communications in Ukraine (asserted as the first country in Europe). Kyivstar, a Ukrainian operator owned by Veon, has become Starlink's partner. The potential customer base for D2D service is estimated at 1.2 million subscribers.

Fig. 13. Starlink system actual data. Source: ITU

In May 2025, SpaceX made its first serious step towards acquiring its own MSS spectrum. It claimed that EchoStar, a satellite operator, was using its S-band spectrum in a very inefficient way and that valuable resource was lying idle. SpaceX urged the US Federal Communications Commission to allow new players into the 2 GHz range and elaborate new rules for the joint use of the spectrum.

After long-lasting proceedings, EchoStar in September 2025 abandoned its plans to create a D2D constellation and repudiated the contract entered into in August with MDA Space for the delivery of satellites. Most importantly, it sold the spectrum to SpaceX: ranges of 1915-1920 MHz and 1995-2000 MHz and ranges of 2000-2020 MHz and 2180-2200 MHz. That’s 50 MHz in total. The transfer of rights is planned for 2027. By that time, the world will already see widely spread user devices of the 3GPP standard in n256 – the band intended for 5G NTN satellite communications.

SpaceX is planning to deploy a new generation Starlink Direct to Cell constellation to ensure broadband communications for smartphones. And already in late September, the operator filed to the FCC a request for a system of 15,000 satellites working in MSS range.

In November 2025, Eutelsat, ESA and Airbus tested the 5G signal transmission via OneWeb satellite. The experiment is claimed to be one of the steps on the way to ensuring uninterruptible global broadband communications for 5G devices. The British startup Open Cosmos in collaboration with Panasonic is working on a preliminary project of a D2D constellation.

The main change in the image of the D2D industry today and the main result of the year 2025 is probably the fact that no players remain here who are only oriented at partner frequencies of mobile network operators. In any case, all active companies have gained in their disposal a spectrum of mobile satellite communications.

Main Title

[1] ITU report “Measuring digital development: Global Connectivity Report 2025”. Facts and Figures 2025, https://www.itu.int/hub/publication/D-IND-ICT_MDD.GCR-2025-4/)

[2] ITU report “The State of Satellite Broadband 2025” https://www.itu.int/pub/S-POL-BROADBAND.31-2025

[3] GSMA report “Spectrum for D2D Public Policy Paper”.

[4] GSOA webinar “The Game-Changer: Direct-to-Device Satellite Connectivity”

[5] Analysys Mason “From orbit to edge: satellite meets cloud in the age of AI”